What’s this blog all about?

To answer that, I go back to my therapist and his recommendation that I have an exit strategy. I’m in my 5th year at my job, a good job, a job I “had to have” during the interview process but what I don’t have is a good answer as to what comes next. What is my plan B after this job.

I am 50 and my hair is grey and the reality is that I am not the cute puppy I once was. And this year my cholesterol went up as did the amount of time I spent in Urgent Care and I have been thinking about what’s next.

As I thought about what was next I envisioned the things I love doing – I love the training for triathlons, in particular long bike rides. Not much time for long bike rides working 40 hours a week. I love volunteer work, particularly with those in recovery, but again not much time for that when I commute 80 minutes a day.

Those are to some extent things that anyone would love, but I don’t think the assignment was – hey think about all the fun things you could do to fill 168 hours a week; I think it is more along the lines of how do you plan to make a living? And as much as that led to me to what I DO want to do, it also led me to what I DO NOT want to do. I don’t want to re-enter the job market at 50, I don’t want to start off in a new industry and I don’t want to leave San Diego.

So for a few months that exit strategy was the topic of conversation in therapy as well as in my journal. Another major topic was stock and option trading, because somehow I had managed to find a therapist who understood what I do and helped reshape my thinking around it. And as I journaled and as we spoke, one day the light bulb went off that I cannot possibly be the only one in this situation and what if – what if I took my journal public and started this blog?

And now I am about a week into it and finding my voice and one piece of feedback I have gotten that maybe I skipped a few steps and risk losing my readers by diving so fast into the technical aspects of options and indexes and blah blah blah. So let’s lay it out slowly.

For years my relationship with money was such that I figured the money tree would never stop sprouting new leaves. I could make money fairly quickly and spend it even quicker. I kept a healthy relationship with debt and but a pretty unhealthy relationship with savings. Every year or so, some 401k advisor type would come in and show the graph with the straight line trending up and to the right if I just put $50 a paycheck in starting at 23 years old I will be a millionaire. That would last a few months and then I would go to Vegas or buy a car I didn’t really need. That was fine in my 20’s but not so fine in my 30’s and at some point I realized I needed to reframe this relationship.

Probably in my 30’s I began buying stocks and accumulating a bit of a portfolio but it wasn’t until my 40’s that I discovered options. A lot of this blog is going to be about options, so I am going to try to lay out what an option is here. And let me say right now – I don’t have a license, I did not go to school for this, I am completely self-taught, all of which is to say don’t sue me.

Basically, an option is a contract that gives you the right, but not the obligation, to buy or sell a specific asset at a set price (the strike price) by a certain date (the expiration date). The simplest example is the Covered Call. This is like the 100-level class of options.

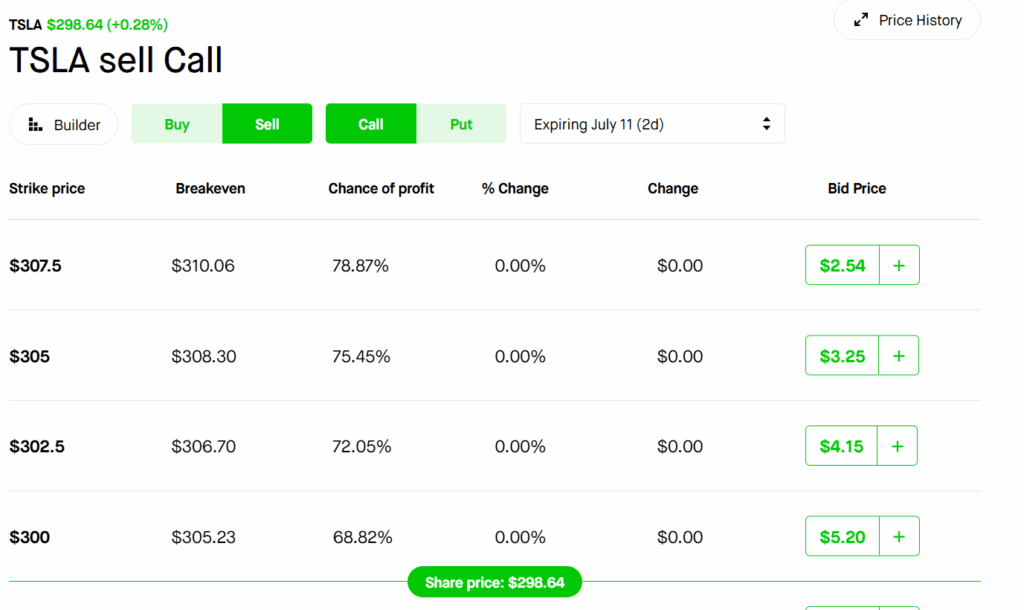

If I own 100 shares of a stock (100 shares is the number you need to execute an Option contract), I can trade an option. So let’s use a real world example. Let’s say I bought 100 shares of Tesla (TSLA) at $300 per share. I can then immediately sell (Write is the term) an option contract for someone to be able to buy those shares from me at a price I choose. Let’s say I am willing to sell those shares at $305 (this is called the Strike Price). I look up the chart and see that I could sell that call contract expiring this Friday (the Expiration Date) for $3.25. Because I own 100 shares, that means I get $325 (the Premium) for being willing to sell those shares at $305. If the stock goes over $305 by Friday, the shares will automatically be deducted from my account. In that scenario not only would I make that $325, I would also make $500 profit on the TSLA stock itself (the difference between the $300 I bought it and the $305 at which I sold it). That is a Covered Call.

Covered Calls are the safest option trade because the downside to Covered Calls is the stock price decreasing. TSLA is a great example of that because the price swings so widely. So in that same scenario, I could buy it at $300, sell that $305 Covered Call (and collect my $325) and then the stock can drop a lot, say to $250. That exact scenario has happened to me before. So in that case, I keep the stock and I go back to the chart and I find another $305 strike price but because the stock is now at $250, the Expiration Date won’t be the next Friday, it will probably be 3 or 4 or 5 Fridays from now. That is the downside of Covered Calls, but if you think about it that isn’t much of a downside.

Each week when I publish my portfolio of Stocks and Options, you will see the way I built it is to have 2-4 Covered Calls expiring every week, trying to make around $200 on each one. I built it this way strategically so that if a stock takes a nosedive I always can Write another Covered Call for as far as 8 weeks out. The whole idea is to make ~$600 per week consistently and reduce my risk.

But it wasn’t always that way, because Covered Calls are not the only option in Options (pun very much intended). It took a lot of wins and losses to get me to this place where reducing risk has become as important to me as building my account balance. That led me to the 1% Plan.

For years I traded and traded and built a large account balance – from $5000 at the beginning to over $150,000. It took losing most of it, rebuilding and finally getting into therapy to help get me to this plan. Before my therapist challenged me to create an exit plan, he forced me to get honest about trading, because it was out of control, or rather it was controlling me.

Over the next few weeks, I will be laying out the trials and errors that led me to where I am today – the 1% plan. The 1% plan is based on the objective of earning 1% per week on my money. And over the next 18 months I will be taking you on my journey to financial freedom, one day at a time.

Over the course of the next 18 months I will document my journey as I carefully work to build $60,000 into $100,000 on December 31, 2025 & $200,000 on December 31, 2026. The idea being that 1% of $200,000 is $2,000 and theoretically that $2,000 covers my very basic monthly nut, so in a real way I am working to create my own salary.

These posts will cover the personal journey over the years to get to this place, the investment basics you need to implement the 1% plan, the successes and failures along the way, some of the fundamentals you will need if you are going to try this on your own and some of the tricks I have taught myself, sometimes to protect myself from myself.

I have a laundry list of character defects but a bucket full of assets too, among them grit, work ethic and a capacity to learn from past mistakes. Why can’t I apply those to this project? This will be a very real-time experience and it’s something of an experiment. By December 31, 2026 we will see together if this works.

What did I need to get started with Options trading?

- A computer. A basic computer works fine. Long term I may want a stronger computer – and there is an entire market devoted to day trading computers (which are basically just gaming computers), but to start you just need a computer.

- A brokerage account with sufficient permissions to trade Cash-Secured Spreads (Level 3 with Robinhood, Level 2 with Schwab). There are many out there but I tend towards the simpler, more consumer-facing brands like Robinhood or Schwab.

- $25,000 (this will keep out of trouble with Pattern Day Trader rules)

- Basic knowledge of investment, in particular Options Trading. I spent a good 2 years reading books, taking online classes, reading blogs and talking to other like-minded people trying to do the same thing I was doing. TD Ameritrade (now Schwab) offered an entire series where you could earn a “certification” in Options trading and I found it very helpful to give me the basics.

- Margin trading permissions (not required, but not having margin trading ability would limit my progress towards building my account balance).

- Basic knowledge of spreadsheets and budget tracking.

- Time. In future posts I will talk about Ironman training/racing and how anyone can do it if they want it enough and devote the time. This is no different. This is not a get rich quick situation; this takes time, consistency and patience. You get out of it what you put into it.

Next week we will dive a little deeper into some of the more complicated Options trades but I will leave it here for now.

Leave a Reply